Executive Summary

Copper prices have breached the 10,000 USD mark, gold prices remain high, and chemical costs are climbing, creating a perfect cost storm sweeping through the PCB (Printed Circuit Board) and PCBA (Printed Circuit Board Assembly) supply chain. This article analyzes the data behind the price surges, identifies the key drivers—including booming AI server and electric vehicle demand—explores the profound impact on industry structure and profitability, and outlines effective strategies for PCB manufacturers to navigate this challenging period, from material substitution to supply chain collaboration.

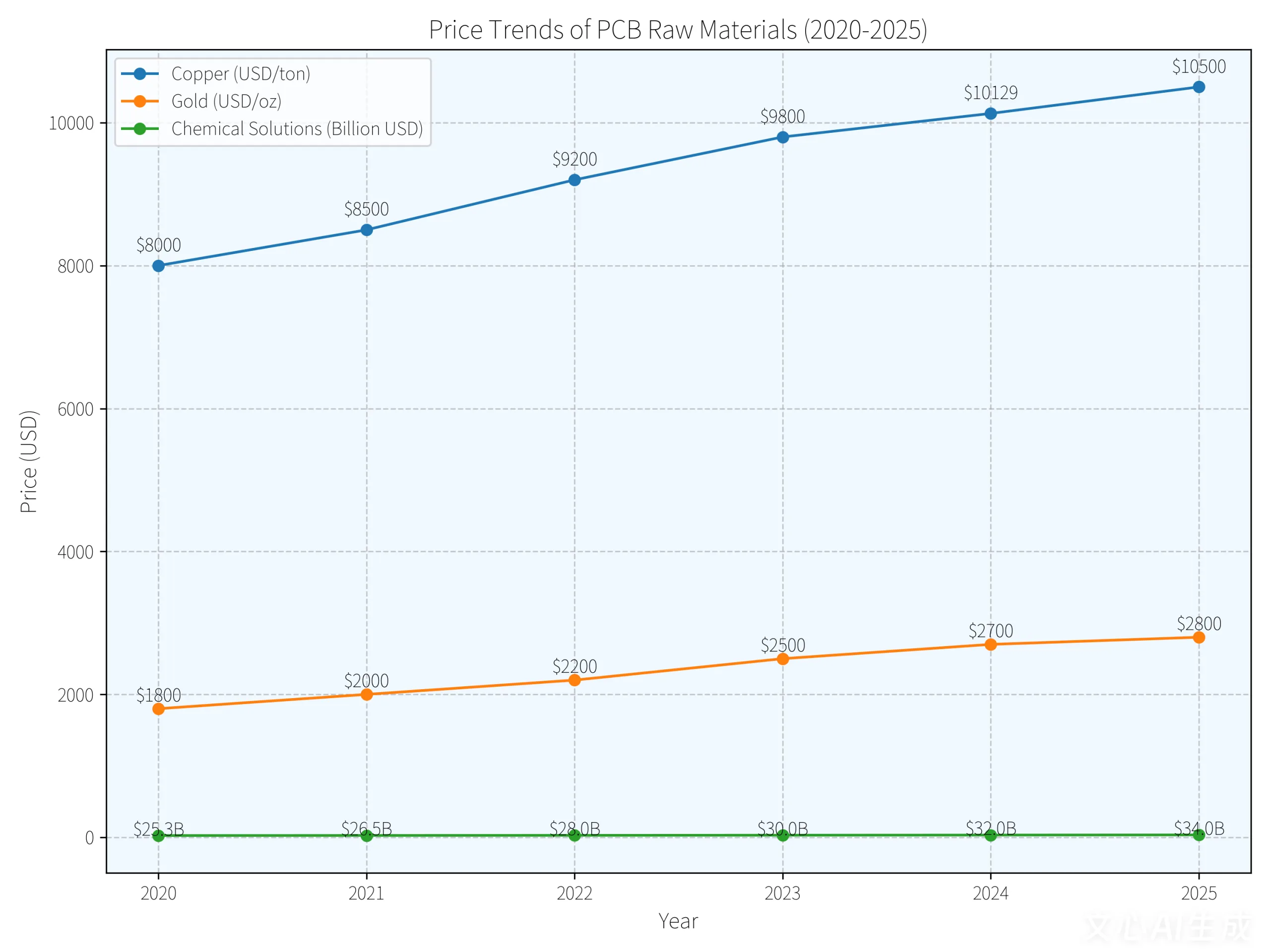

01 Price Volatility: Data Reveals Soaring Raw Material Costs

Printed Circuit Boards (PCBs), often called the “mother of electronic systems,” are essential for nearly all electronic devices. However, the cost structure of this fundamental component is currently under immense pressure.

Raw materials constitute approximately 60% of a typical PCB’s cost structure. The most significant single category is the copper-clad laminate (CCL), accounting for 27.31% of the total cost. The primary materials for CCLs—copper foil, epoxy resin, and glass fiber fabric—are all experiencing sustained high prices, directly driving up PCB manufacturing costs.

Copper, a key benchmark, continues its upward trajectory. Current monitoring data shows the price of Electrolytic Copper (1#) has reached 85,430 RMB/ton, a 5.2% increase from late September to mid-October alone. More concerning is that international copper prices have already surpassed the 10,000 USD milestone, with LME copper futures briefly exceeding $11,000 per tonne in early October.

Beyond copper, other essential materials are also seeing widespread price increases. Electronic glass fiber cloth prices are up 12% year-on-year, with some suppliers announcing a comprehensive 20% price hike for their glass fiber products starting in August. Chemical products are also contributing to the cost pressure. The price of Sulfuric Acid (98%) increased by 1.6% month-over-month, while Caustic Soda (Liquid Alkali, 32%) rose by 1.1%. The rising cost of these basic chemicals directly increases the production cost of essential PCB chemical solutions.

02 Root Causes: The Drivers Behind the Raw Material Price Surge

This wave of raw material inflation is not without cause; it is the result of multiple converging factors.

Fundamental Supply-Demand Imbalance

The global PCB market is projected to reach $83.7 billion in 2025, a 4.2% year-on-year growth. Demand from high-value-added sectors like servers, AI computing equipment, and new energy vehicles continues to climb sharply, now accounting for over 35% of total industry revenue.

AI Computing Demand Boom

The explosive growth in AI computing power demand has driven substantial expansion in the high-end PCB market. Industry data reveals that global AI server shipments surged by 68% year-on-year, spurring a higher-than-anticipated demand surge for HDI boards and packaging substrates. The average layer count for PCBs used in high-end AI servers has increased from 18 layers in 2023 to 32 layers in 2025, representing a substantial leap in technical requirements and value.

Automotive Electronics Expansion

Vehicle electrification is another major catalyst. Global sales of new energy vehicles are expected to reach 18.2 million units in 2025, with a penetration rate exceeding 24%. The average PCB value in a pure electric vehicle is 3.7 times that of a traditional internal combustion engine vehicle, dramatically stimulating PCB market demand.

Supply Chain Bottlenecks

Capacity constraints are a critical issue. The industry relies heavily on imported high-end PCB manufacturing equipment, with Japanese and German companies holding over 80% of the global market share. Equipment delivery lead times have extended from 9 months in 2023 to 15-18 months in 2025. This inability to rapidly expand capacity to meet demand has resulted in a backlog of orders exceeding $12 billion.

03 Industry Impact: From Cost Transmission to Market Restructuring

The ripple effect of raw material price inflation is permeating throughout the entire PCB industrial chain.

Squeezed Profit Margins

With raw materials representing such a high portion of the Bill of Materials (BOM), price fluctuations directly impact corporate profitability. While some leading companies have managed to improve gross margins by optimizing product mix and client portfolios, most small and medium-sized enterprises (SMEs) are facing increasingly difficult conditions.

Shifting Competitive Landscape

The industry’s competitive dynamics are undergoing a crucial adjustment. Leading manufacturers are consolidating their advantages through technological upgrades and capacity expansion, while some SMEs, pressured by costs, are gradually exiting the low-to-mid-range market. Data shows the combined market share of the global top 10 PCB manufacturers rose to 52% in 2025, a 3-percentage-point increase from 2024.

Product Mix Evolution and Price Divergence

The product structure is changing noticeably. Price increases are most pronounced for high-end PCB products, particularly those used in AI servers, High-Density Interconnect (HDI) boards, and high-frequency, high-speed PCBs. In 2025, prices for high-end PCBs rose 37.8% year-on-year, with delivery lead times stretching from the traditional 4-6 weeks to 12-16 weeks.

A significant price divergence between different application areas is emerging. The price per square meter for AI server PCBs has jumped from $800-$2,000 for traditional servers to $30,000-$50,000, an increase of 15-25 times. This structural change is pushing the PCB industry towards a higher value-added transformation.

04 Survival Strategies: How PCB Companies Can Navigate the Crisis

Confronting the relentless surge in material costs, PCB manufacturers are deploying multi-pronged operational strategies to engineer market breakthrough solutions.

Material Substitution

In response to soaring copper prices, the electronics industry is actively preparing material substitution strategies. Alternatives like aluminum and steel are being evaluated to reduce production costs. Industry experts estimate that adopting alternative materials can effectively lower production costs and curb copper demand, helping to stabilize global market prices.

Technology Upgrade and Product Mix Optimization

This is a common choice for leading firms. Capitalizing on the surge in AI server PCB demand, relevant manufacturers are boosting the technological content of their products, achieving a 2-3 percentage point year-on-year increase in gross margins. High-end products, such as 20+ layer multi-layer boards and 6+-order HDI boards, command significant price premiums and have become a crucial profit source.

Supply Chain Collaboration and Cost Sharing

Building closer partnerships with upstream and downstream partners to jointly manage cost volatility is becoming increasingly important. Some large PCB manufacturers are even engaging in equity participation and joint ventures to secure their upstream raw material supply, thereby enhancing supply chain stability.

Process Efficiency and Recycling

For specialized materials like chemical solutions, optimizing usage efficiency and implementing recycling programs are effective cost-control measures. By improving processes like electrodes copper plating (PTH) and increasing chemical utilization rates, manufacturers can effectively reduce the manufacturing cost per PCB panel.

Flexible Pricing Mechanisms

Companies are also actively revising their pricing models, establishing more flexible price adjustment strategies. For instance, some are linking product selling prices directly to raw material indices, with regular adjustments to reflect cost changes more rapidly.

05 Future Outlook: When Will the Price Surge Subside?

The critical question for the industry remains: when will this storm end?

Short-Term Persistence

The near-term pricing momentum is expected to remain intact, with industry consensus forecasting sustained upward pressure on premium-tier PCB products through Q4 2025, potentially extending into subsequent fiscal periods. With the adoption of next-generation M9 materials starting in 2026 and scaling in 2027, prices for high-end PCBs are projected to rise a further 30%-50%.

Long-Term Relief Through Technology

In the long run, technological iteration will be key to alleviating cost pressure. The PCB industry is undergoing a materials revolution. The performance leap from M8 to M9 materials will bring enhanced product capabilities, partially offsetting the impact of rising raw material costs. Simultaneously, the rise of domestic raw material suppliers will help improve supply chain stability.

Sustained Demand Drivers

From a demand perspective, AI, electric vehicles, and 5G/6G communication will remain the three core engines driving PCB industry growth. With global AI server shipments growing 68% year-on-year and new energy vehicle PCB penetration surpassing 75%, these high-growth sectors will continue to pull demand for advanced PCBs.

Industry Consolidation

Structural adjustment and increased market concentration will define the coming years. Chinese manufacturers, leveraging industrial cluster effects and cost-control capabilities, have seen their market share break 40% for the first time, becoming the core growth driver for the global PCB industry. For companies unable to adapt to this transformation, exiting the market or being consolidated may be an inevitable outcome.

Copper prices continue to fluctuate at high levels, and R&D into aluminum alternatives is accelerating. Walking through a PCB factory, the hum of machinery remains, but the cost structure of every single circuit board has irrevocably changed.

“This price surge is an industry shake-out,” remarked a factory manager with twenty years of experience. “Companies that competed solely on low price will be eliminated. Those who remain must master core technologies.”

The global PCB market is forecast to reach $96.8 billion in 2025. The survivors of this cost storm are poised to claim a larger share of this growing pie.